August 16, 2019 | Institutional Perspectives | 6 min read

The Highs of Low-Volatility Investing

By March 9, 2009, the subprime mortgage crisis had knocked nearly 57% off the S&P 500 Index’s highs of 17 months prior. These were dark days. Although it has now been over ten years since markets bottomed, the scars remain and still impact investor behavior. With markets again near all-time highs, many are looking for ways to generate returns with less risk.

Against this backdrop, over the past decade companies involved in defensive, low-volatility (“low vol”) sectors such as consumer staples, utilities, real estate and telecommunications have commanded investors’ attention due to the consistency of their revenues even through economic downturns. These low-volatility sectors have been popular, but our experience is that popular areas of the market tend to become expensive. We are concerned that low-volatility equity strategies are at risk of repeating this pattern.

What is risk?

Many investors (and academics) simplify the concept of risk to being all about volatility, or the amount that an investment’s value oscillates over time. Legendary investor Warren Buffett warns against this practice, though, writing in his 2014 Letter to Shareholders that ”volatility is far from synonymous with risk. Popular formulas that equate the two terms lead students, investors and CEOs astray.”

He goes on to suggest that these short-term movements are unimportant, preferring investors focus instead on “attaining significant gains in purchasing power over their investing lifetime,” something a diversified equity portfolio can provide.

A tangible definition of risk is that you don’t have enough money to pay for your plans whether that’s your retirement, your child’s education, or end-of-life medical care. Investors can find themselves here for a variety of reasons, including not starting early enough, investing too conservatively, or by suffering permanent impairment to their capital along the way.

For the purposes of this article, we will adopt the industry reference of “volatility equals risk,” but in practice we see things much as Buffett does: short-term volatility is a source of opportunity, not risk. Strong fundamentals that enable the creation of long-term value for shareholders is what matters.

The Rise of Low Vol

In recent years, investors have deployed increasing funds into low-volatility stocks, and active and passive funds, with the hope of minimizing “risk” (volatility) while still generating an attractive return. Figure 1 shows that the popularity of low-volatility funds which were virtually non-existent prior to the financial crisis has soared over the last several years, with over $25 billion flowing into products in the area in Canada alone.

Figure 1: Growth of Canadian Low-Volatility Funds

This influx of demand has helped low-volatility stocks outperform the market in recent years and led, in turn, to a “low-risk, high-return” investment outcome. This phenomenon, coined the “low-volatility anomaly,” upsets a key of tenet of portfolio theory: that higher risk companies higher returns.

The S&P 500 Low-Volatility Index tracks the performance of the 100 stocks in the S&P 500 with the lowest volatility (the index is rebalanced quarterly). Figure 2 shows the outperformance of this Index relative to the broader S&P 500 Index over the past five years. The highlighted portion of the chart represents times of increased outperformance by low-volatility stocks, which corresponds to declining interest rates (more on that below). Low-volatility stocks earned an 11.9% annual return over the period while the S&P 500 rose 10.7%. It is easy to see how this would thrill risk-averse investors!

Figure 2: Performance of Low-Volatility Index vs S&P 500 Index, 2014-2019

Popularity Has a Price

Valuation multiples allow investors to determine how “expensive” a company is relative to its peers, the overall market, and its own history. One of the most common multiples used by analysts, the price-to-earnings (P/E) ratio, tells you how much you’re paying for each dollar of earnings of the company. High ratios can signal a stock (or sector) is overvalued, as was the case with the dot-com bubble in the late 1990s.

Investors have traditionally been willing to pay higher P/E ratios for companies with higher-than-average future growth expectations. Low-volatility stocks, however, which are now consistently being priced at high multiples, do not carry the same promise of growth. This suggests many investors are willing to pay a premium for the perceived security these investments provide, despite their modest growth expectations.

What Has Been Behind This Phenomenon?

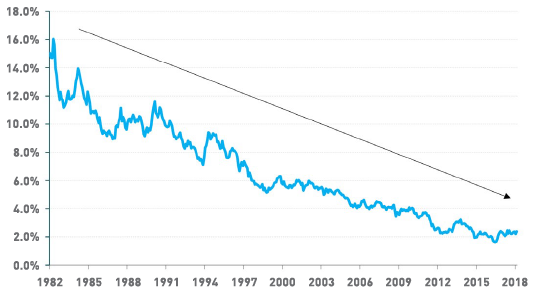

One factor which helps explain the “low-volatility anomaly” is the interest rate environment in which we find ourselves. Figure 3 shows how dramatically the yield on a 30-year Government of Canada bond has declined over the last three decades, including a halving from 4% to 2% in the last eight years.

Interest rates matter to defensive stocks because they are often stable, mature, cash-flow generating businesses that pay solid dividends. With interest rates at historic lows, high dividend-paying stocks look even more attractive than they have in the past. In fact, many investors are choosing to own higher yielding stocks in place of bonds to leverage their attractive dividends. Unfortunately, in doing so they are forfeiting the downside protection that bonds offer and replacing them with equity securities that are still highly-correlated with the risks inherent to the overall stock market.

Declining rates also benefit companies with debt financing in their capital structure. Given the ower (perceived) business risk and higher predictability of cash flows for companies in the mature stage of their life cycle, they often take on higher levels of debt. Being more leveraged also increases sensitivity to changes in interest rates, which in a declining rate environment has allowed highly leveraged companies to steadily refinance their outstanding debt at lower rates, further augmenting their earnings.

Figure 3: Long-term Government of Canada Bond Yields

The Campbell Soup Company is a notable example of a low-volatility company that has been around for over 150 years. Its consumer staples businesses of soups and simple meals, affordable snacks, and beverages are non-cyclical in nature because no matter the health of the economy or the stock market, people have to eat. Having reached the “maturity” stage of the firm life-cycle, Campbell’s total debt-to-equity (D/E) ratio as of June 30, 2019 was 7.5x. In comparison, the D/E of the S&P 500 Index was 1.2x. If interest rates remain at their lows, or begin to rise in years to come, highly-leveraged companies like Campbell’s will not continue to benefit from declining rates like they have over the last three decades. In fact, their debt levels could become problematic.

“Past Performance is Not Indicative of Future Results”

A common blind spot for investors is to pursue what has performed well and dismiss what has performed poorly, a trend known as “performance chasing.” Paying a premium for expensive, low-volatility stocks is no exception.

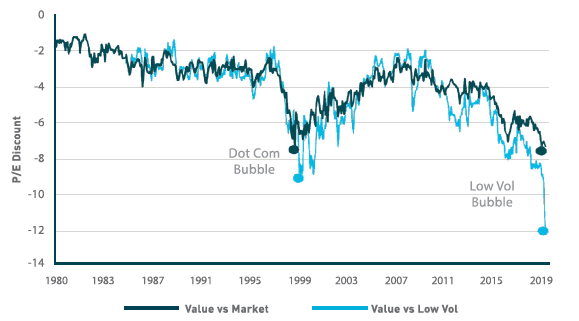

A recent study conducted by JPMorgan indicated the valuation gap between value stocks and low-volatility/defensive stocks is at historically high levels. Figure 4 shows the difference in P/E multiples between value stocks and both low-vol stocks and the overall market. When the dot com bubble peaked, for example, value stocks were trading at P/E multiples that were nearly eight multiple points lower than the tech-frenzied overall market (green line). The blue line shows how value stocks have lagged low vol as the latter’s bubble has inflated over the last few years. Value stocks are currently trading at P/E ratios in the low-to-mid teens, while many low-volatility stocks are changing hands at over 20x earnings.

Benjamin Graham, Warren Buffett’s professor and mentor, and author of The Intelligent Investor once said, “The intelligent investor is a realist who sells to optimists and buys from pessimists” not someone who dives head-first into an already bullish sector. While we do not know when the low vol phenomenon will turn, we know that at some point, it will. In the meantime, as always, our firm will maintain our investment approach, and seek value where others do not.

Figure 4: Valuation Gap Between Value and Low-Volatility Stocks

IMPORTANT NOTE: This article is not intended to provide advice, recommendations or offers to buy or sell any product or service. The information provided is compiled from our own research that we believe to be reasonable and accurate at the time of writing, but is subject to change without notice. Forward looking statements are based on our assumptions, results could differ materially.

Reg. T.M., M.K. Leith Wheeler Investment Counsel Ltd.

M.D., M.K. Leith Wheeler Investment Counsel Ltd.

Registered, U.S. Patent and Trademark Office.