May 15, 2023 | Planning Matters | 6 min read

Using a Flow Analysis in Estate Planning

Matching intentions and results is the truest definition of success in estate planning, and one strategy to achieve this is what I call a "flow analysis." Where does my property go when I pass away? Where does it “flow”? I like the concept because for me it conjures the image of a creek that appears to head in directions by outside forces. It just happens.

With estate planning, property will “flow” to people based on the plans put in place and the law’s interpretation of those plans. That may not always be what you expect, so it’s useful to map things out in advance to confirm you’re headed in the right direction.

I see that most frequently with beneficiary designations done badly, so let’s go through an example.

Mary and Her Three Kids: Designated Beneficiary & Disability Planning

Mary is a widow with three adult children. She would like the three to share equally in her estate upon her death, with special consideration for 35-year-old Johnny, who has a long-term disability and lives with her in the family home in Alberta.

Johnny will require a trust for his lifetime (sometimes referred to as a “Henson Trust”) because his disability prevents him from understanding finances and investing, or making appropriate decisions about when or how to use money from the trust. Johnny's disability is not so severe that he can't function (with supports) in the community. He goes out with friends and has a part-time job that he gets to on local transit. But Mary is concerned that he would be vulnerable regarding his funds. He has a big heart and will give money to anyone who asks.

Mary has named Johnny as the designated beneficiary for her RRSP as she heard there may be some tax benefits in doing this.

As her daughter Laura helps her with financial decisions (and on the advice of the bank, which said it would make things easier), she added Laura’s name to her main checking and savings accounts.

In her Will she has a Henson Trust for Johnny. Then, she wants Laura and her other son Tom get their share of the estate as an outright gift (that is, no trust).

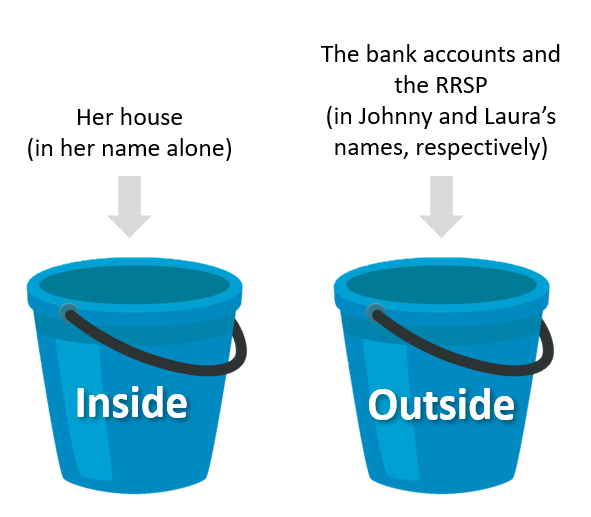

Will this work out as planned? Let’s do a "flow analysis" for Mary to find out. Step one is determining what is “inside” and what is “outside” the estate.

In meetings with clients, I often use the analogy of buckets. Think of a regular bucket with a handle, the kind you may have in your utility closet or garage. For most persons, there are two buckets (more for more complicated estates, but let’s keep it simple). One would be "inside" the estate and the other is outside." In Mary’s case, which of her assets are inside the estate and which are outside?

What we can conclude from these buckets is that the estate won’t be divided equally as Mary intends. Why?

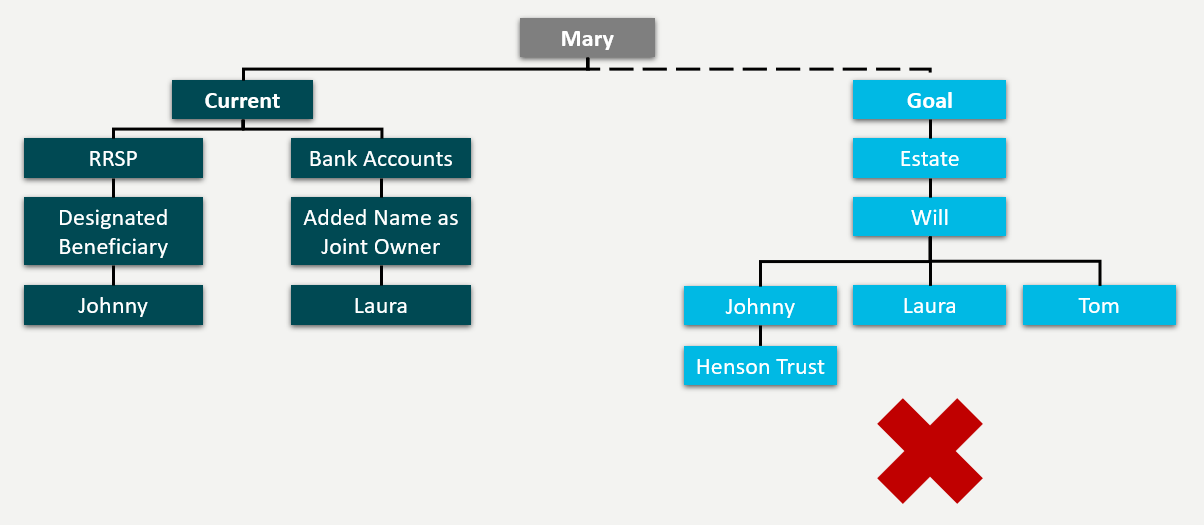

Figure 1: Mary’s Flawed Current Plan

On Mary’s death, the RRSP will go to Johnny directly and will not be part of his trust. This is due to the beneficiary designation in the RRSP. It does not matter what Mary's Will stipulates; the most-recent beneficiary designation

will govern1.

On top of that, the accountant advises that the RRSP will go to Johnny but the tax arising from the deemed disposition on Mary's death will be included in income on Mary’s final tax return. That will generate taxes owing which will be an obligation of the estate (even though the estate did not receive the proceeds from the RRSP).

Note that Johnny is living in the house and wants to stay there. But there are no other assets in the estate to pay the tax. There is discussion about putting a line of credit on the house to pay the taxes.

The bank accounts will go to Laura who is listed as a joint owner on the accounts with the bank. On the assumption the bank will treat the accounts as a true joint account, the end result is that they will go to Laura as the surviving joint owner. Now, maybe she shares these accounts with her siblings... but maybe she does not.

Laura hints that this was Mom's way of paying her back for all the time spent helping Mom over the years and Mom intended her to have these accounts and not share them. She recalls that being discussed with the banker. She does not think this money should be used to pay for the funeral or the tax from the RRSP.

So What Would a Flow Analysts Suggest Mary Do?

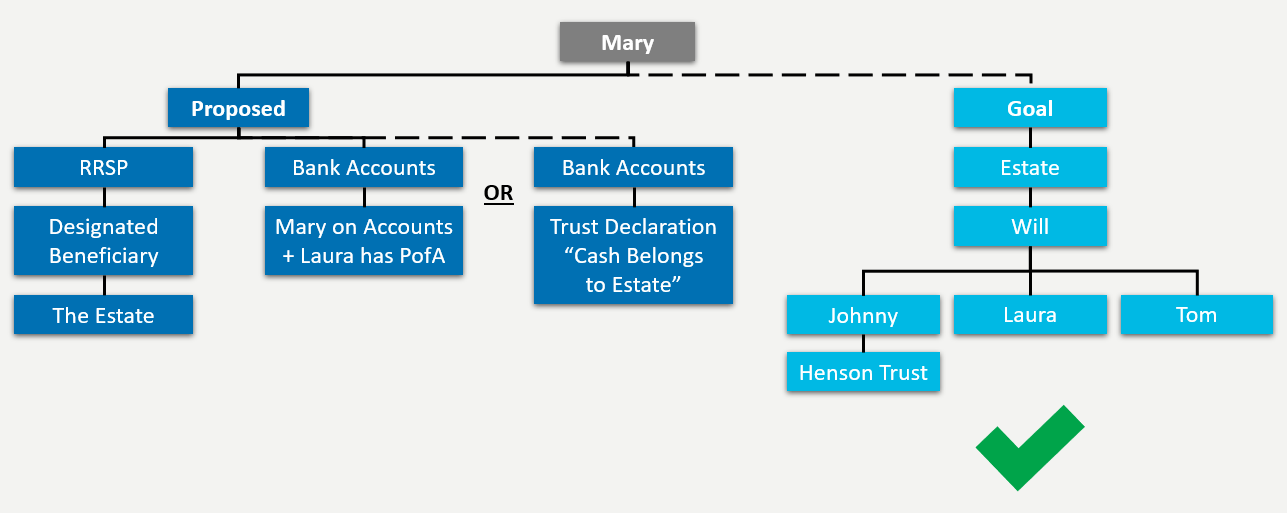

The recommendations to Mary would be to change the beneficiary designation to "the estate" so there is money to pay for the taxes and the funeral. What is left over can be divided equally and Johnny's share will form part of his Henson Trust. This will ensure he also stays on government supports, which in Alberta is referred to as the Assured Income for the Severely Handicapped (or abbreviated to “AISH”).

Jointly held bank accounts fall outside the estate and are not controlled by the executor. By undertaking a “flow analysis” in advance, Mary has the option to take Laura off the bank accounts and, as a better alternative, to grant her a Power of Attorney so Laura can assist her in managing her regular bill payments and investments. Keeping the account in Mary’s name would allow the funds to be controlled by the executor and distributed in accordance with her last Will.

If Mary wishes to keep the banking arrangement she has, she and Laura could put in writing that Laura will use those funds as estate assets and distribute in accordance with the terms of Mary's last Will (sometimes called a trust declaration). In other words, Laura confirms that the funds are not hers alone.

The matter of compensating Laura could be itemized separately so that she is treated fairly (but not with the option of receiving the full contents of the bank accounts).2

Figure 2: A Better Approach to Achieving Mary’s Wishes

Mary can thus avoid an unintended result, along with the costs of litigation – which include time, money, and relationships. All three children can share equally in her estate, as desired, and Johnny can be assured a secure financial future.

With the simple planning of a flow analysis, tax paid can be mitigated, control of property can pass to the desired people and, more importantly, Mary’s wishes can be carried out.

About the Contributor

Gordon VanderLeek, BA, LLB, TEP (gordon@vanderleeklaw.ca) has been practicing law for over 35 years and is the founding lawyer of VanderLeek Law in Calgary. His practice focuses on solving problems and educating in the areas of estate planning, estate administration and trust law. Gordon is the parent to 5 adopted children and enjoys spoiling his one grandchild. When he gets some time off, he enjoys hiking, golf, kayaking, paddle boarding and camping with his wife, Annie. He is sometimes seen exploring gravel roads and trails on his adventure motorbike or trying to grab a wildlife photo as he pretends to be a National Geographic photographer.

1Not applicable for Quebec residents.

2The information above is relevant to Alberta residents. Alberta is a low probate fee jurisdiction so funds flowing through the Estate are generally not a concern (the cost is capped at $525). Other provinces may charge a percentage fee for the probate application to be processed or have other costs/implications specific to your jurisdiction of residency. Please seek legal advice applicable to your situation to better understand the potential costs, implications and/or strategies.

NOTE: The information contained herein should not be treated by readers as legal advice and should not be relied on as such. We suggest you seek legal advice for your personal situation.