February 16, 2023 | Quiet Counsel | 7 min read

Outlook 2023, Part I: Inflation

In Part I of our two-part Outlook series, we go through our current thinking about inflation and interest rates. Be sure to check out Part II to learn our outlook for the chances of an economic recession, as well as prospects for fixed income and equity markets.

Let’s face it, 2022 was a brutal year for investors.

Visit our website, to download previous Newsletters and read our latest Insights.

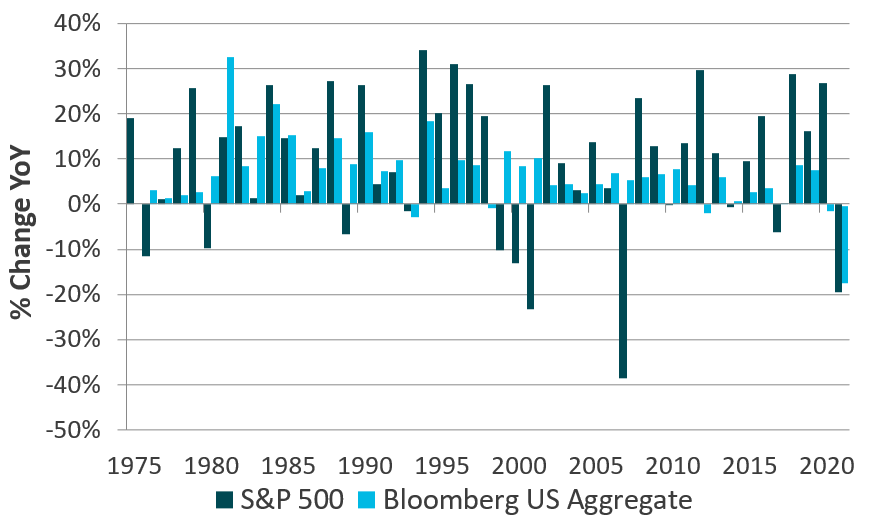

As the global economy emerged from the pandemic, a combination of factors led to the inflation that emerged. Supply chain bottlenecks, pent-up demand, big spending by governments, and a war in Europe that disrupted energy markets all played roles. After an overly slow initial response, central banks were then forced to hike interest rates more aggressively than originally expected, prompting a sell-off across all markets including equities, government bonds, corporate bonds, real estate, infrastructure, and even gold and digital currencies. It was the first year since 1994 that both equities and bonds posted negative returns.

Figure 1: Annual returns of US stock and bond markets, 1975-2022 (USD)

There are many reasons for the market correction in 2022 but at the core is the increase in government bond yields, which were pushed up by interest rate hikes. Investors use these yields (referenced in this context as the “discount rate”) as an input in the models they use to price all financial assets. When the discount rate goes up, the estimate of fair value of stocks and bonds goes down, and vice versa. This discount rate had been steadily declining since the early 1980s, and was intentionally pushed down by central banks after the 2008 global financial crisis and the 2020 pandemic. When inflation finally emerged in 2022, the “punchbowl” was removed and the discount rate implied by government bond yields rose. The result was that capital market valuations were adjusted lower across the board.

So where are government bond yields headed in 2023 and beyond? The pessimistic view is that inflation and bond yields are now on an upward and endless spiral; however, while inflation may remain elevated in 2023 we have a more sanguine outlook. A longer term perspective at this juncture is warranted.

Inflation

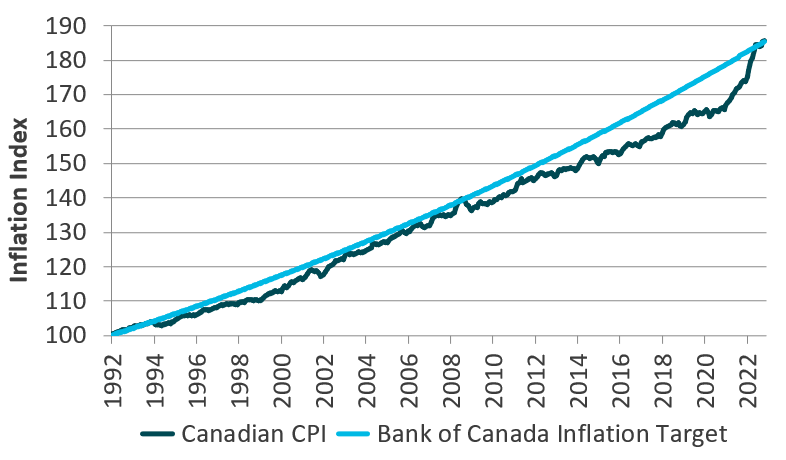

Consider this: since the advent of inflation targeting in Canada in 1991, the Bank of Canada has consistently run short of its 2% target. As Figure 2 shows, when inflation finally caught up to the 2% run rate in mid-2008, it was then buffeted for the next 15 years as consumers and businesses spent their money paying down the debt of that crisis. Today is the first time since the advent of central bank inflation targeting that the Bank of Canada’s inflation-fighting credentials have really been tested.

“...while inflation may remain elevated in 2023 we have a more sanguine outlook. A longer-term perspective at this juncture is warranted.”

Figure 2: Canadian inflation versus the Bank of Canada inflation target, 1991-2022

We believe the Bank of Canada has sufficient levers to bring inflation under control, by forcing demand destruction and a recession or otherwise. However, in our view the more important question is whether the factors that caused consumer prices to run below the Bank of Canada’s target inflation rate for the past 30 years – demographics, technology, globalization, and leverage – are likely to return in the future.

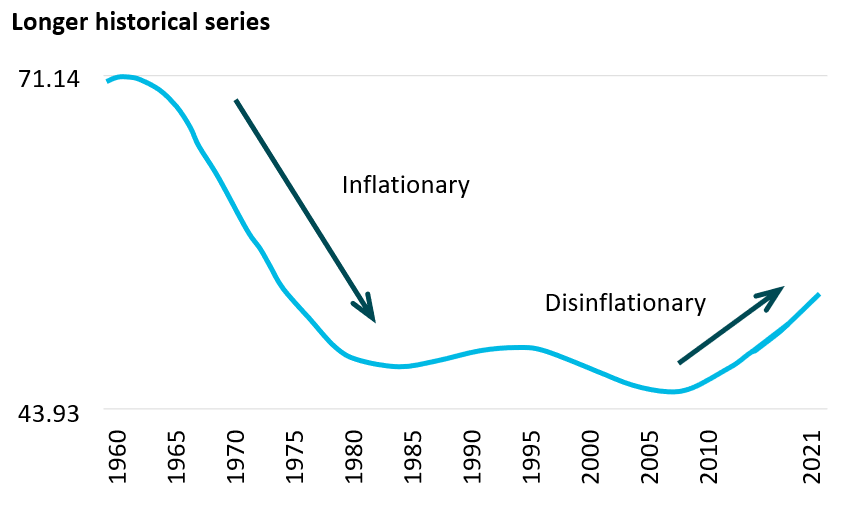

Demographics. Stats Canada expects our natural population growth (ex-immigration) to slow in the coming years due to our aging population and low fertility rate, and may even turn negative by the 2050s. As a result, despite immigration, Canada’s working-age population will struggle to support their retired elders (known as the dependency ratio – shown in Figure 3). Outside of Canada, the outlook is even worse as the IMF predicts developed world population growth will turn negative by 2030. Our view is these demographic trends will likely put downward pressure on inflation over the next decade and beyond.

Figure 3: Canada’s dependency ratio, 1960-2021

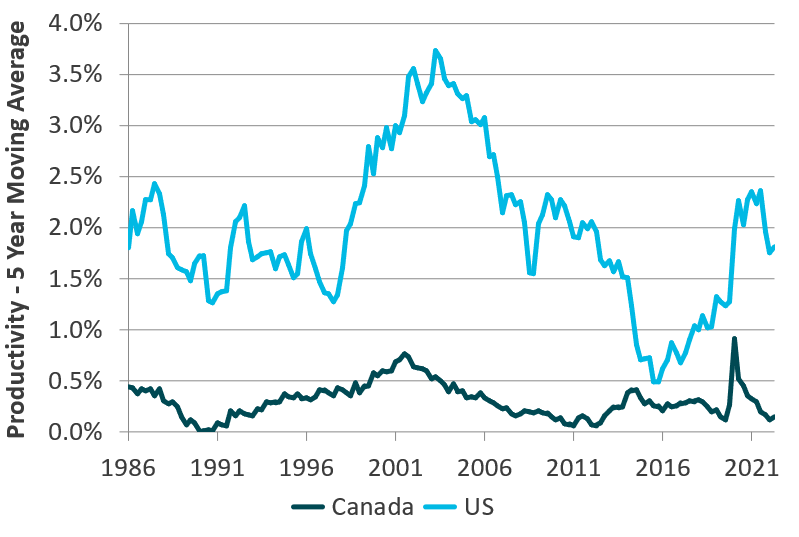

Technology. Disruptive technologies and innovation can improve productivity, and this is expected to continue happening globally. Higher productivity lowers costs, pushing down inflation. However, as Figure 4 shows, the annual productivity gains have been in decline since the 2000s, and Canada’s gains have been particularly anaemic relative to the US.

Figure 4: Productivity gains in Canada and the US, 1986 - 2021

While technology can improve productivity, it needs to translate into real gains to have the desired downward effect on inflation. Given Canada’s low productivity gains, it’s unclear it will enjoy the same “disinflationary” effects (reduction in the rate of inflation), relative to the US and elsewhere. Further, while Canada would benefit from lower global prices, weak productivity would ultimately feed into a weaker Canadian Dollar, which would push up inflation in Canada specifically1.

Globalization. Since the 1970s, world trade (as a percentage of global GDP) has risen from 25% to 60%, as manufacturing was offshored to countries with a lower unit labour cost. However, the disinflationary impact of this move peaked in the late 2000s, and was only a marginal contributor to disinflation in the 2010s. Furthermore, the 2020 pandemic has prompted a major rethink of global supply chains and will likely result in increased onshoring of manufacturing (under US President Biden, this trend has accelerated in recent years). However, our view is the impact from any reversal is likely to be modest in the near term while labour costs abroad remain more cost-effective.

Leverage (debt). In most of the developed world, the global financial crisis caused households to “deleverage,” or put their extra cash into paying down debt rather than, say, buying new cars or appliances. As mentioned above, this created disinflationary pressures for the next 15 years. Where are we now in that cycle?

Again, the outlook here is not straightforward. Households in the US went through a painful deleveraging, however Canadian households (and the housing market) were relatively immune. The picture today is very different, with Canadian private sector indebtedness near record highs. While Canadian banks’ balance sheets are in substantially stronger positions, the impact of any deleveraging (caused by higher rates / housing market corrections) is likely to be deeply disinflationary. When considered together, our view is the long-term inflation outlook remains more uncertain and two-sided than today’s headlines might suggest. Productivity remains elusive and globalization seems to have run its course. However, neither are expected to suddenly reverse and become significant drivers of inflation. Meanwhile, demographic headwinds and the prospect of a Canadian deleveraging remain. We therefore do not necessarily think high inflation is a foregone conclusion over the next decade.

Rather, our view is that inflation likely peaked in June at 8.1% in Canada, and we are therefore close to the end of the interest rate hiking cycle. Relative to the US, Canadian inflation is falling for more reasons than lower energy prices, and core inflation measures appear to be heading back towards target. The implication for the capital markets is that the adjustment up in the discount rate (and down in valuations) has likely already largely occurred.

What matters for markets now is the adjustment of the real economy to these higher borrowing costs (generally, by slowing investment in growth), sufficient to push inflation toward the Bank of Canada’s 2% target.

So far, the Bank of Canada appears likely to finish its interest rate hikes at around 4.5%, which is 0.5% to 0.75% lower than the US. The main reason for this lower rate is Canadians are more interest rate-sensitive given both our high household debt (think: auto loans or credit cards) and exposure to mortgage debt (including floating-rate, which has inflicted the pain immediately).

Persistently above-target inflation along with extensions or expansions of central banks’ high interest rate policy pose the single largest threat to both the economy and capital markets.

How will inflation impact capital markets in 2023 and beyond?

Read Outlook 2023, Part II to find out.

1There are several reasons why Canadian productivity has lagged behind other developed countries over the past decade, including lower investment in research and development; a lack of competition in some sectors which reduced incentives to innovate; a less-diversified economy heavily reliant on natural resources; smaller companies (which are generally less productive due to their lack of access to financing, skills, and technologies); and an aging population with low immigration rates, as a smaller, older workforce has less productivity gains than a larger, younger one.

IMPORTANT NOTE: This article is not intended to provide advice, recommendations or offers to buy or sell any product or service. The information provided is compiled from our own research that we believe to be reasonable and accurate at the time of writing, but is subject to change without notice. Forward looking statements are based on our assumptions, results could differ materially.

Reg. T.M., M.K. Leith Wheeler Investment Counsel Ltd.

M.D., M.K. Leith Wheeler Investment Counsel Ltd.

Registered, U.S. Patent and Trademark Office.

Photo credit for cover image: Mike Wallberg.